Paid UA on the alternative app stores was the buzz around ChinaJoy in Shanghai. The biggest gaming exhibition in Asia attracted more than 41,000 B2B visitors this year including Flexion’s Michael Hu. He reports that recent changes in some ad networks are generating a lot of excitement among developers.

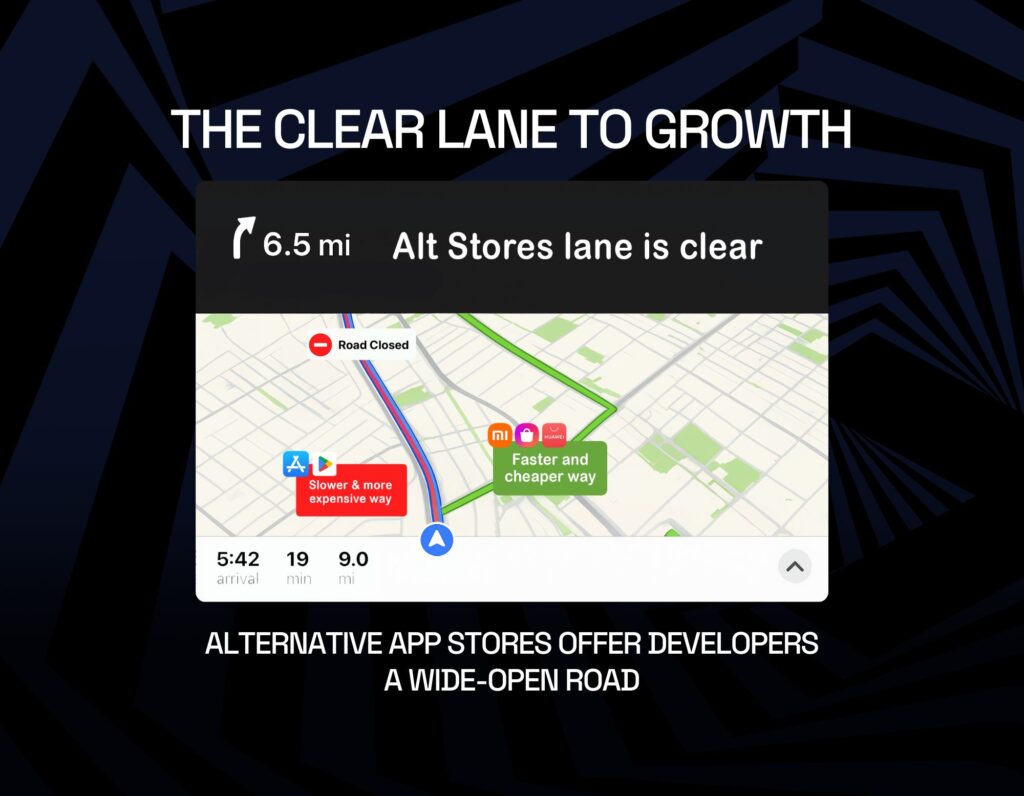

Efficiency is the name of the game for developers when it comes to attracting new users. But the skyrocketing costs of paid user acquisition (UA) on Google and Apple is forcing many to look at other approaches.

Paid UA has been so firmly enmeshed with the Google and Apple ecosystems that it has been difficult to imagine any other approach. But these days, I’ve seen some cases where the cost of a game installed on Google or Apple exceeds $10. That’s just not sustainable. Something had to give.

In the last 12 to 18 months, some ad networks (notably Moloco and Liftoff) have spotted this changing dynamic and looked to expand their coverage. This was the talk of ChinaJoy because what it means is paid UA is now viable on the alt stores, offering access to a relatively untapped market of users. And these entirely new users arrive at your game at a much lower cost.

This is not only making paid UA through the alt stores possible, it’s making it positively attractive.

For now, at least, advertising through the alt app stores is less competitive and so the costs are lower. But the alt stores also offer a much more reasonable revenue split which means better margins for the developer from new users who pay. This is turning RoAS (Return on Ad Spend) calculations on their head.

Part of the reason this subject came up so often at ChinaJoy in particular is that in many parts of South-East Asia, alternative stores actually do better than their mainstream rivals at engaging audiences. Local app stores typically support region-specific payment, lowering friction for players, making it more likely they’ll pay.

If this is all starting to sound like a no-brainer, be warned. There are some challenges.

While the ad networks have responded quickly to the pressures on developers, MMP*s are still catching up. This means you can do paid UA campaigns on the alt app stores but finding out how well each one is doing is currently tricky. For example, Samsung has the Galaxy Store and Instant Play but, if your game is on both, there are technical challenges in separating the measurement data from the sources. MMPs, platforms and ad networks will need to work together to overcome this type of friction. But the pressures on paid UA are such that it may not be long before we see improvements. In the meantime, the RoAS could be so good that it’s worthwhile for developers to find their own way around the issues.

There are also tech challenges in measuring how new users convert to revenue. You may need to configure S2S (server to server) integration manually, currently.

Finally, if you want to gain new users through 5 different alt app stores, you’re probably going to need to learn 5 dashboards and 5 sets of tools. This may also be worth the investment but in due course we can expect third-party dashboards to make UA more consistent across market channels.

Although developers will need to weigh the risks and rewards of paid UA through the alt stores, there are benefits to being an early adopter. Ad costs are currently low but are likely to rise as these markets inevitably become more competitive. But you also gain a strategic advantage in terms of being ahead of the curve in learning about this new approach to UA. Developers can also gain useful experience which may benefit the evolving D2C market. Currently, this is relying on web stores and only support out of game payments but the future will look very different when distribution and 3rd party IAP becomes mainstream.

* MMP = Mobile Measurement Partner, which provides third-party tools and services to help game developers measure, analyse, and optimise their UA.